Southeast Asia’s pet products industry is booming, and opportunities abound for brands looking to expand into this fast-growing region. Pets have become an integral part of daily life for many consumers, but entering the Southeast Asian market comes with challenges. Diverse regulations, fragmented legal frameworks, underdeveloped logistics and infrastructure, and various cultural and regulatory factors create additional challenges for companies aiming to enter and grow in the local market.

Southeast Asia Pet Market Overview

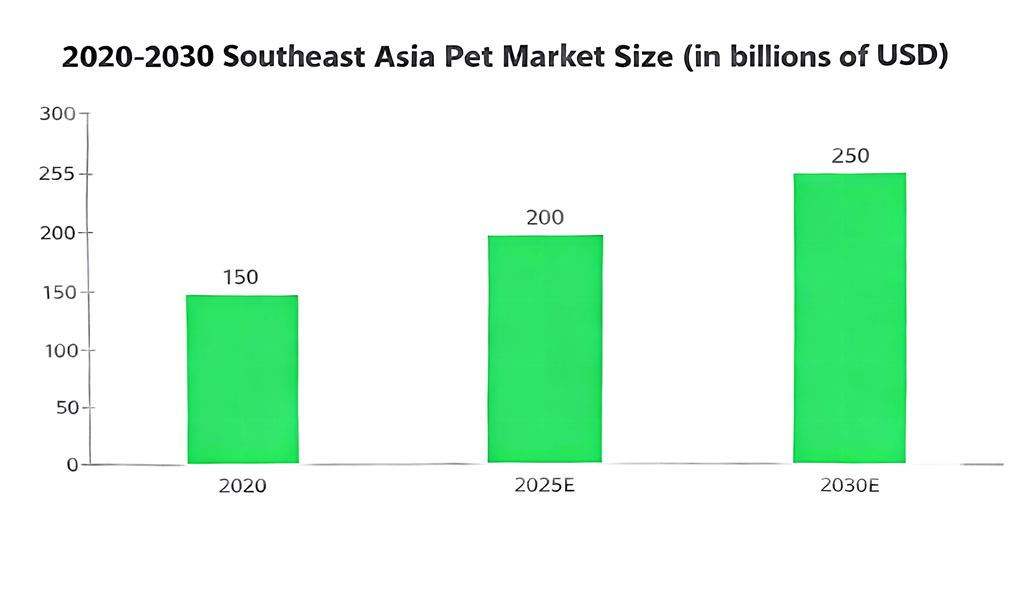

Southeast Asia, home to 690 million people, is one of the world’s fastest-growing emerging markets. By 2025, the region’s pet market is expected to experience explosive growth. Industry forecasts indicate the market has already surpassed $20 billion USD, with a 15% annual growth rate. With a large and young consumer base, rapid urbanization, and a rising trend toward emotional spending, Southeast Asia has become a hotspot for international brands in the pet sector.

However, the region shows significant market segmentation. Countries like Indonesia, Thailand, and Malaysia stand out in terms of size, pet ownership, and consumer preferences.

Indonesia: A Cat-Centric Market Driven by Islamic Culture

According to Future Market Insights, Indonesia’s pet market is projected at $2.8 billion in 2025, growing to $6.8 billion by 2035, with a CAGR of 9.5%. About 67% of Indonesian households own pets, with cats dominating at 69%, while dog ownership is only 13%. Among younger consumers aged 16–24, 73% keep cats, reflecting a generational shift toward feline companionship.

Indonesian Pet Culture

Around 87% of Indonesians are Muslim, and within Islamic culture, dogs are often considered “unclean,” resulting in cats being the preferred pets. In 2022, the country had 4.8 million cats and only 919,200 dogs, a trend expected to continue by 2026.

Government Policies Impacting the Pet Industry

- Promoting pet health products and encouraging companies to produce high-quality pet food, supplies, and supplements.

- Implementing strict regulations on pet food production, including compliance with food safety laws, regular inspections, and quality control.

- Supporting e-commerce platforms like Shopee, Tokopedia, and Lazada, which help expand access to pet products across the country.

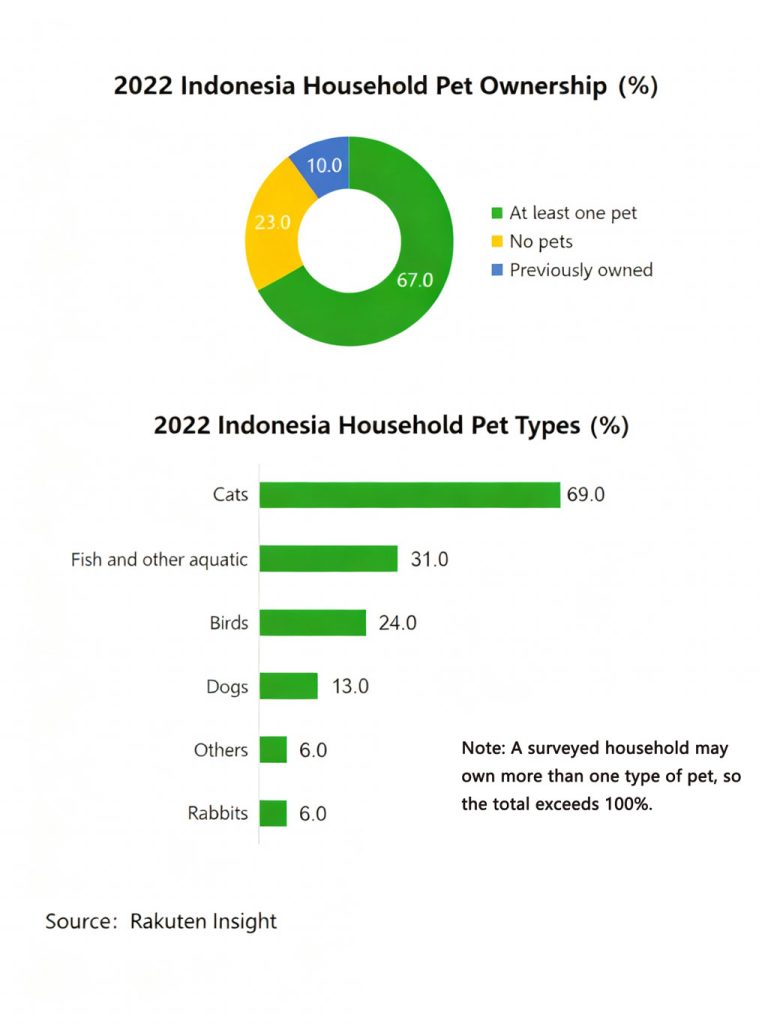

Pet Ownership Structure

In 2022, 67% of Indonesian households had pets:

Cats: 69%

Aquatic pets: 31%

Birds: 24%

Dogs: 13%

(Source: Rakuten Insight)

Market Size

The Indonesian pet market is projected at $2.8 billion in 2025, reaching $6.8 billion by 2035 (CAGR: 9.5%). Pet food sales in 2023 were $1.85 billion, expected to reach $2.16 billion by 2025, growing at a 7.55% CAGR through 2029.

E-Commerce Development

In 2024, Shopee Indonesia sold 228 million pet items totaling $362 million. Peak sales occurred in October (29.88 million items, $53.12 million), while September saw peak sales revenue ($55.8 million, 28.38 million items). Shopee dominates with 74.1% of pet food sales, followed by Tokopedia (18.7%) and Lazada (6.87%).

Samarchronicle: Growth of Cat Food Sales in Indonesian E-Commerce

Product Segmentation

- Pet food: Cats (36.37% of units, 47.83% of revenue), dog food (12.19% of units, 28.37% of revenue).

- Pet accessories: Aquatic equipment leads in sales (43.4%) and revenue (40.36%).

- Pet healthcare: Vitamins and supplements dominate sales (48.2%) and revenue (47.01%).

- Litter & hygiene: Dog training pads lead in revenue (63.5%), cat litter next (9.57%).

- Pet apparel & accessories: Collars lead in sales (79.5%) and revenue (48.78%).

- Pet grooming: Hair care dominates sales (62.8%) and revenue (73.25%).

Thailand: Humane Trends Driving Pet Services Market

TTB Analytics reports Thailand’s pet market at 75 billion THB in 2024, a 12.4% YoY increase. Food consumption is up 15.8%. Dogs and cats remain dominant, with fish, birds, rabbits, and rodents also popular.

Thai consumers’ spending distribution: 45% food, 32% services, 23% products. Average spend per shopping trip was 177.3 THB in 2022, highest among dog owners. Young single women are key consumers of tech-enabled pet products. Pet grooming (bath & haircut) accounts for 61% of service usage.

Pet Culture in Thailand

Over 95% of Thais are Theravada Buddhists, influencing attitudes toward animals, which are viewed as living beings deserving respect. Many consider pets as family members, sometimes granting them “pet monarch” status. Aging populations and more single-person households amplify pets’ role in companionship.

Government Policies Impact

- Animal Protection Act: Safeguards animal welfare and prohibits cruelty.

- Veterinary Profession Act: Requires registered vets to follow standards, raising healthcare quality.

- Promoting pet-friendly public spaces, restaurants, and hotels.

- Regulatory improvements in pet trade and exotic pet management, including the Dangerous Animal Control Act.

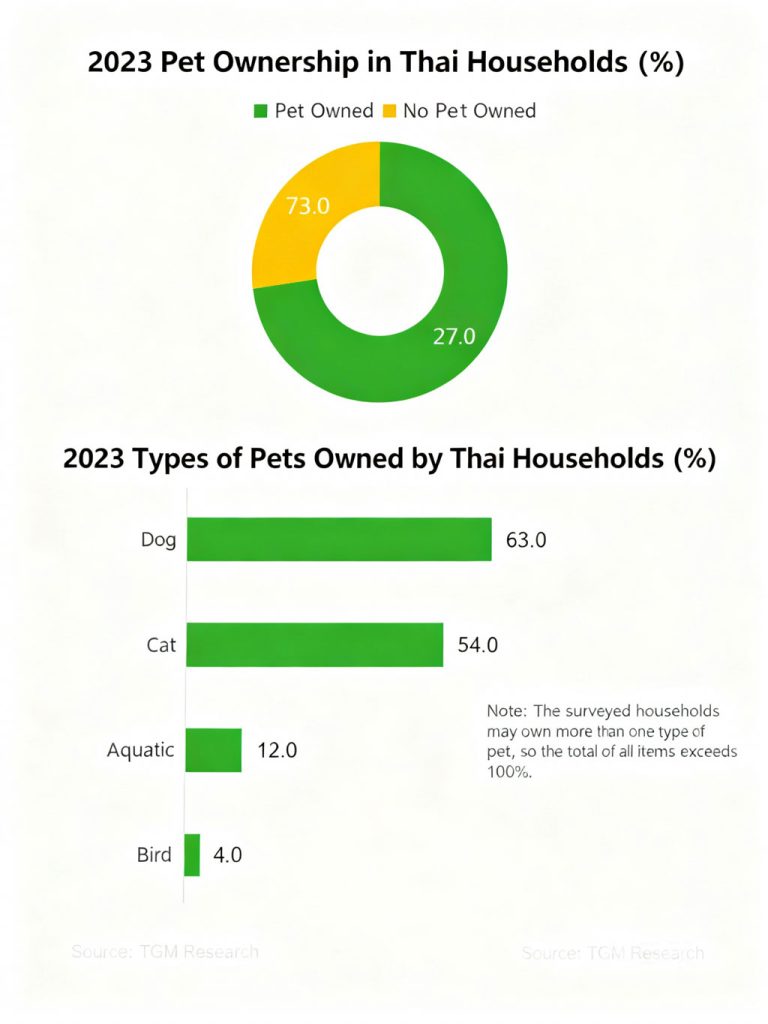

Pet Ownership Structure

In 2023:

73% of households had pets

Dogs: 63%

Cats: 54%

Aquatic pets: 12%

Birds: 4%

(Source: TGM Research)

Market Size

2023: $1.46 billion

2024 forecast: $2.2 billion

2029 projection: $3.35 billion (CAGR: 10.87%)

Pet food expected $39.46 million in 2024 (CAGR: 17%), pet products $20.25 million (CAGR: 17.3%). Pet services, including grooming, healthcare, and boarding, are rapidly growing. Veterinary services: $197 million (CAGR: 21.7%), pet care services: $19.6 million (CAGR: 16.7%).

E-Commerce

Shopee Thailand 2024: 80.33 million items, $364 million.

Peak monthly sales: September: 10.51 million items, $43.81 million; December: $59.9 million, 10.01 million items.

Product Segmentation

- Pet accessories revenue: 22.96%

- Food: 55.29%

- Accessories: Aquatic devices lead in units (25.73%) and revenue: pet furniture leads (33.73%).

- Health: Vitamins top units (55.4%) and revenue (68.89%).

- Litter & hygiene: Cat litter leads units (44.53%),

Malaysia: A High-End Market Driven by Online Channels

According to Euromonitor International, the Malaysian pet industry reached a market size of USD 430 million in 2023 and is expected to grow to USD 450 million by 2024, with a compound annual growth rate (CAGR) of 5.8%. Urbanization at 78.7% has driven pet ownership to 51.1%. Cats are the most popular, accounting for 60.0%, followed by dogs and aquatic pets at 36.0% and 25.0%, respectively. In terms of pet product preferences, pet food accounts for 52.8% of the total market. Cat food dominates the pet food market, accounting for over 60%, while dog food accounts for approximately 31.8%.

Pet Culture in Malaysia

About 53% of Malaysians practice Islam. Influenced by religion, Malays tend to prefer cats, as they are considered clean and sacred in Islamic culture. In contrast, the Chinese community is more inclined to keep dogs, as dogs symbolize loyalty and protection in Chinese culture.

Policy Impact on the Pet Industry in Malaysia

Malaysia’s policy environment has played an important role in both promoting and regulating the pet industry. The government supports sustainable growth through economic policies, trade agreements, regulatory frameworks, and attention to animal welfare.

- By participating in the Regional Comprehensive Economic Partnership (RCEP), Malaysia has further opened its pet service market. For example, veterinary services under RCEP have been opened to foreign investment, allowing joint ventures to provide veterinary services, significantly boosting the pet medical services market.

- The government has implemented a series of regulations on pet ownership. For instance, dog owners must obtain written consent from neighbors to apply for or maintain a pet license. Moreover, strict regulations are in place for imported pet food and medicines, requiring compliance with food safety certifications (such as HACCP, ISO 22000) and relevant qualifications.

- The rapid development of e-commerce and widespread internet access have created new sales channels for the pet industry. Online platforms such as Shopee and Lazada have become major channels for pet product sales, driving growth in online sales.

Pet Ownership Structure in Malaysia

In 2023, 51.1% of Malaysian households owned pets, with 26.4% having multiple pets. Among the 48.9% of respondents without pets, 26.2% expressed interest in owning one. Cats were the most popular, accounting for 60.0%, followed by dogs and aquatic pets at 36.0% and 25.0%, respectively.

Malaysian Pet Market Size

The pet industry reached USD 430 million in 2023 and is projected to grow to USD 450 million in 2024, with a CAGR of 5.8%.

The pet food market was valued at USD 259 million in 2023 and is expected to reach USD 282 million by 2025, with an annual growth rate of 9.54% (CAGR 2025–2029).

Development of E-Commerce Channels

In 2024, Shopee Malaysia recorded 59.14 million pet product sales, generating USD 203 million in revenue.

- In September 2024, sales peaked at 7.06 million items with revenue of USD 23.48 million.

- In December 2024, revenue peaked at USD 35.72 million with sales of 6.94 million items.

Sales by Product Category

- Pet Food: Cat food accounted for 46.69% of sales volume, cat treats 29.52%, dog food 6.44%; in terms of revenue, cat food 58.20%, dog food 20.56%, cat treats 5.93%.

- Pet Accessories: Aquarium equipment accounted for 38.86% of sales volume, pet furniture 23%, pet toys 11.81%; revenue share: pet furniture 35.98%, aquarium equipment 30.9%, bowls & feeders 10.28%.

- Pet Health: Vitamins and supplements 40.13%, veterinary services 31.38%, flea & tick products 22.82%; revenue share: vitamins and supplements 56.44%, veterinary services 23.18%, flea & tick 14.85%.

- Cat Litter & Toilets: Cat litter & litter boxes 45.05% of sales volume, dog training pads & trays 16.55%, bags & scoops 13.62%; revenue share: cat litter & litter boxes 70.01%, dog training pads & trays 13.49%, small pet litter boxes & sand 5.91%.

- Pet Apparel & Accessories: Pet clothing 53.28% of sales volume, neck accessories 28.71%; revenue share: pet clothing 62.18%, neck accessories 16.78%.

- Pet Grooming: Hair care 58.22% of sales volume, oral care 13.54%, nail care 7.99%; revenue share: hair care 69.40%, oral care 10.28%, nail care 4.57%.

Singapore: Pet Humanization Trends Driving Services and Premium Consumption

According to a report by Deep Market Insights, the pet care market in Singapore is estimated to reach USD 1.02 billion in 2024. Dogs and cats remain the mainstream pets, but in compact urban environments, cat ownership is on the rise. According to Pet Fair Southeast Asia, in multi-pet households in Singapore, cats account for approximately 51%. Consumer preferences in pet food, products, and services are also shifting: pet food remains dominant, especially imported and premium-formula products, which are seeing strong growth. U.S. brands already hold about 23% of the Singapore cat and dog food market.

Pet Culture in Singapore

Pet owners in Singapore increasingly view their pets as “companions” or “family members” rather than simply “animals.” In high-density urban housing (such as HDB flats or apartments), pet-keeping spaces are limited, which has promoted trends toward smaller pets and indoor living. Pet owners tend to choose pets suitable for apartment living, such as cats, small dogs, and small animals. Pet health, hygiene, behavioral training, and smart device applications are becoming increasingly important.

Policy Impact on Singapore’s Pet Industry

The Singaporean government has gradually improved regulations on pet ownership and the pet industry:

- Pet registration and microchipping are required, with new rules for pet-keeping in public housing (HDB) and other environments.

- Animal welfare and public health are incorporated into policy considerations, with regulations covering pet stores, pet boarding, and pet certification services.

- Pet-friendly facilities, such as pet cafés, grooming shops, boarding and daycare services, are increasing in cities, creating conditions for the expansion of the pet service market.

Pet Ownership Structure in Singapore

According to YouGov 2023 surveys, about 34% of adults in Singapore own pets. Distribution by pet type:

- Dogs: ~13% of respondents

- Cats: ~12%

- Fish: ~7%

- Rodents (hamsters, guinea pigs, gerbils): ~3%

- Birds and rabbits: ~2%

Although the overall proportion of pet-owning households is not as high as in some other countries, dogs and cats remain the dominant pets in Singapore.

Singapore Pet Market Size

In 2024, the total pet care market in Singapore—including food, products, and services—is estimated at USD 1.02 billion (approximately SGD 1.4 billion, based on estimated exchange rates). Deep Market Insights cites 2024 as the base year.

- Pet food: Projected revenue for 2025 is approximately USD 102 million.

- Pet accessories: The market size in 2024 is around USD 113.8 million.

- Pet insurance: The segment is estimated at USD 104.4 million in 2024.

The market is expected to continue growing in the coming years, driven by pet humanization, service adoption, and the integration of online and offline channels.

E-Commerce and Retail Development

Online channels are becoming one of the main shopping scenarios for pet food and products in Singapore. Pet Fair Southeast Asia reports that about 45% of pet food purchases are made through online platforms. Traditional retail, such as specialty pet stores and pet supermarkets, remains significant, but e-commerce, social commerce, and subscription services are emerging as new trends.

Product Category Sales Trends

- Pet Food: High proportion of imports, limited local production; consumers are willing to pay a premium for functional/health-focused products. U.S. and European imports are growing rapidly.

- Pet Products: Smart, design-focused, and customized products are popular among urban pet owners, such as smart feeders, pet furniture, indoor toys, and environmental monitoring devices.

- Pet Services: Grooming, daycare/boarding, behavioral training, and health check-ups are growing rapidly.

- Pet Insurance: With longer pet lifespans and increased awareness of health management, pet insurance is a growing segment.

Pet Consumption Upgrade Driving Premiumization and Diversification

1. Consumption Upgrade Driving Premiumization and Diversification

Food Innovation: Demand for functional foods (probiotics, joint health formulas) and natural/organic pet food is surging. Insect-protein cat food from Indonesia and fish-based pet food from Thailand have become bestsellers. By 2025, the Southeast Asian pet food market is expected to surpass USD 5 billion, with mid-to-high-end products (USD 1–3/kg) accounting for over 60%.

Smart Pet Products: Automatic feeders and environmental monitoring devices are growing over 40% annually, with Thailand’s smart pet products exhibition area expected to expand by 50% in 2025.

Service Market Emergence: Veterinary care (CAGR 15%-25%), grooming, and insurance (penetration <5%) are emerging growth areas. The premium pet care market in Jakarta, Indonesia, is projected to reach USD 1.21 billion by 2026.

2. E-Commerce and Social Marketing Reshaping Channels

Southeast Asia’s e-commerce GMV is expected to reach USD 186 billion in 2025, with pet categories experiencing rapid growth. Shopee and TikTok Shop contribute over 60% of sales.

Short-video “influencer seeding” activates young consumers. In Indonesia, TikTok cat food sales account for 58.8%, while pet apparel monthly sales in the Philippines exceed 100,000 units.

According to Bain & Company, Southeast Asia’s e-commerce CAGR is projected at 15.68% in 2025. Although e-commerce penetration continues to rise, offline channels still dominate. In 2023, over 50% of consumers purchased pet products through specialty stores, with Indonesia’s offline share reaching 70% and the Philippines’ supermarkets/convenience stores leading. Online, Shopee and Lazada are the main platforms. Thailand’s 2023 pet market on e-commerce exceeded USD 138 million, with pet food contributing over 50% of sales and showing high repurchase rates.

3. Technological Innovation and Sustainability

Digital Services: Remote consultation apps and smart health-monitoring devices optimize user experience. Thailand’s AI diagnostic coverage in veterinary services has increased by 30%.

Eco-Friendly Transition: Demand is rising for biodegradable cat litter and pet beds made from recycled materials. Companies are accelerating ESG strategies, such as carbon-neutral palm oil supply chains in Malaysia.

Strategies to Capture the Southeast Asian Pet Market

1. Strengthen Supply Chain and Compliance

- Localized Warehousing: Establish overseas warehouses in Indonesia and the Philippines to shorten delivery cycles and reduce logistics costs.

- Compliance Investment: Apply in advance for product certifications in Southeast Asian countries (e.g., Vietnam’s Ministry of Agriculture sales permits) to avoid customs delays.

2. Precise Positioning and Layered Market Strategy

- Premium Market: Focus on organic pet food, smart devices (automatic feeders, smart water dispensers), and eco-friendly products to meet local preferences for quality and technology.

- Emerging Market: Focus on cost-effective dry food, pet toys, and basic supplies (feeders, cages), combined with localized packaging and marketing.

3. Digital and Social Marketing Penetration

- Leverage platforms like TikTok, Facebook, and Instagram for brand promotion and product marketing. Use creative videos and user engagement to boost brand awareness and customer loyalty.

- Develop localized content strategies based on cultural and language characteristics. For example, create pet care videos tailored to local customs or publish content related to local festivals and pet events to engage consumers.

If you are currently in or planning to enter the Southeast Asian market and are looking for trending products, contact Shengkang. Let’s explore the Southeast Asian pet products market together, seize opportunities, and create success!

Data Sources

Data in this report is collected and organized from national statistical agencies, IMF, Rakuten Insight, Statista Market Insights, Euromonitor, and other publicly available online platforms.